The Federal Reserve is holding steady for now, with markets increasingly expecting a rate cut in March 2026 as inflation shows signs of cooling. Strong labor data has dampened the likelihood of near-term easing, but if inflation continues to recede or the job market weakens, a March cut could very well happen.

Why Inflation Trends are Pivotal for Fed Decisions

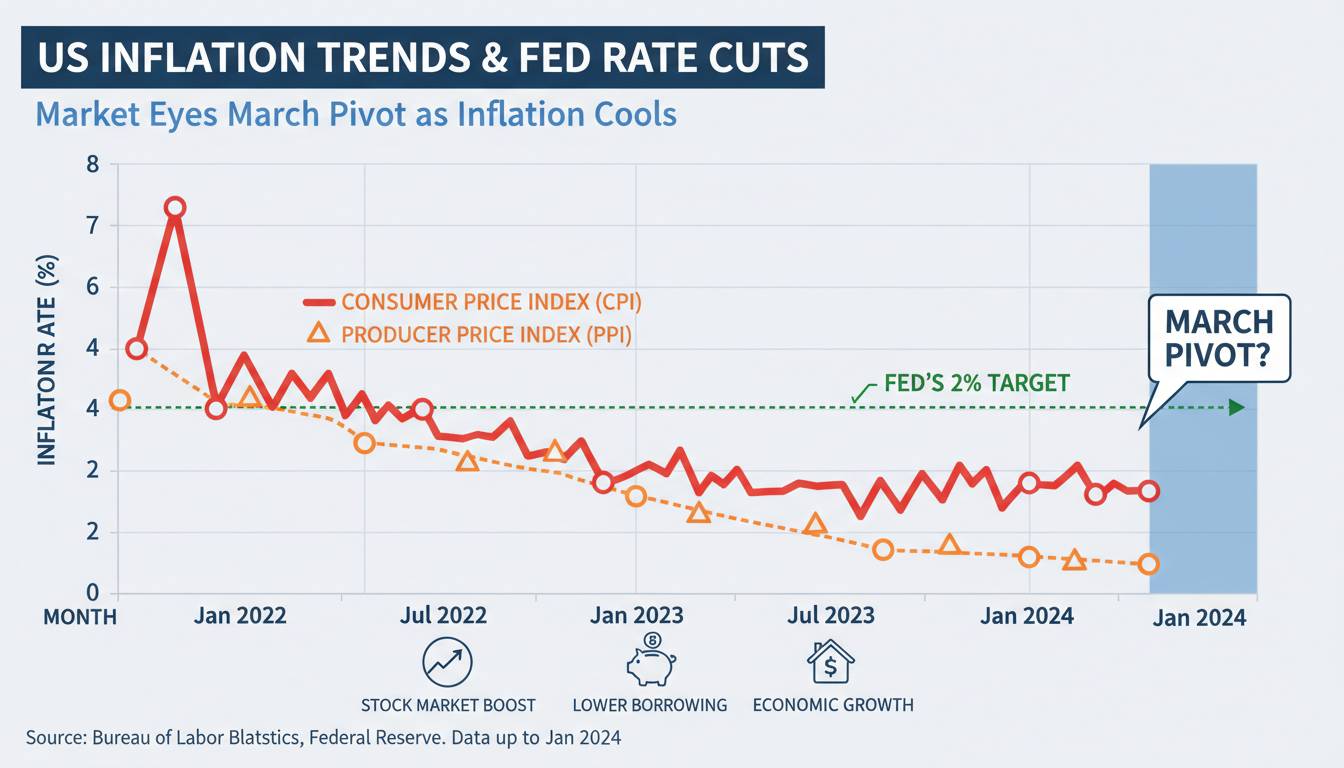

But inflation isn’t quite at the Fed’s 2% target yet. Headline CPI settled around 2.7% in December, down from higher levels but still above ideal. Core inflation remains stubborn too, holding at about 2.6%. That’s better than earlier, but policymakers need more convincing progress to pull the trigger.

Recent January data continues to ease the pressure. Reports show headline inflation near 2.5%, matching five-year lows, while core inflation also hovers around 2.5%. This shift bolsters hopes that the Fed might loosen its grip—but timing remains data-dependent.

Labor Market Strength and Its Influence

Strong jobs data complicates cut expectations. January added a solid 130,000 jobs, unemployment dipped to ~4.3%, and wages are rising—signs of a resilient job market. Fed officials, like Beth Hammack and Lorie Logan, remain cautious; they argue policy isn’t too restrictive yet.

Still, one voice—Governor Stephen Miran—leans dovish, suggesting that deregulation and other factors may allow room for rate cuts. But the consensus is clear: inflation needs to weaken further or jobs must soften noticeably before easing occurs.

What Analysts and Markets Are Expecting

A growing number of forecasts point to a March pivot. Goldman Sachs anticipates rate cuts in March and June, potentially ending 2026 with rates between 3.0% and 3.25%. JPMorgan sees more caution—markets expect no move in March, but strategists leave open the possibility of one cut in 2026.

Other forecasters echo that slower, more deliberate path. Morgan Stanley, for instance, has pushed its first expected cut to March due to inflation risks tied to tariffs. Barron’s reports trading markets anticipating cuts throughout 2026 down to 2.75–3.0%, while Fed officials suggest a flatter approach.

S&P Global captures the crux: without a marked weakening in labor, cuts may not come until summer—or possibly later. As of late December, CME futures priced in about a 46% chance of a March cut. And more recent consensus has shifted some expectations to cuts in June and September instead.

Summary Comparison of Forecasts

| Source | Outlook for 2026 |

|———————–|—————————————————|

| Goldman Sachs | Cuts in March & June; terminal at 3.0–3.25% |

| JPMorgan | No cuts in March; one potential later in 2026 |

| Morgan Stanley | First cut in March; cautious due to tariffs |

| Markets/Futures | ~46% chance of March cut; some now expect cuts in June or later |

| Fed Officials | Prefer slower pace; need more data clarity |

What Needs to Fall into Place for a March Cut?

Currently, inflation is cooling, but not at the Fed’s pace. Labor is firm, adding uncertainty. Analysts agree there’s a delicate mix of factors needed before easing:

- Core inflation must decline further toward 2% sustainably.

- Labor indicators—job additions, participation, layoffs—must show strains.

- Disruptions, like tariffs or fiscal stimulus, must not reignite price pressures.

As Nationwide economist Oren Klachkin notes:

“It’s going to take clear labor market deterioration… the Fed is on hold until Warsh takes the helm.”

So, if the data in February and early March confirms both cooling prices and weakening employment, the Fed could feel confident enough to act.

Conclusion

The bottom line? Markets are leaning toward March 2026 as the potential onset of rate cuts, driven by easing inflation. At the same time, a strong jobs market tempers that view. Analysts and Fed watchers are balancing two scenarios: a cautious March pivot versus a more conservative pause until signs of labor softness emerge later in the year.

Remain alert. Inflation and labor data over the next few weeks will determine whether March becomes the pivot or just another hold.

FAQs

Will the Fed definitely cut rates in March 2026?

Not guaranteed. Markets price about a 45–50% chance of a March cut, but it hinges on meaningfully lower inflation and signs of labor weakening. JPMorgan sees cuts likely later, while Goldman Sachs still expects one as early as March.

What inflation level would persuade the Fed to cut?

Fed officials are eyeing core inflation moving toward 2%; current levels of ~2.5–2.7% are not low enough. Continued declines across key inflation metrics would strengthen the case.

Is the labor market slowing enough for cuts?

Not yet. While some weakening cropped up in late 2025, January still showed strength. Cuts may wait until clear deterioration, like rising jobless rates or sustained payroll drops.

Could we see rate cuts later in 2026 instead?

Yes. Many forecasts now shift cuts toward June or even September, reflecting the Fed’s cautious stance and data-dependent approach.

What risks could delay cuts further?

Persistent inflation from tariffs or fiscal stimulus could push back easing. Additionally, a strong economy or fresh inflation upticks might keep the Fed on hold longer.

Who influences whether cuts happen?

The FOMC sets policy. While Powell remains chair until May, incoming leadership like Kevin Warsh could sway decisions. Still, cuts require broad committee agreement, not just one person.

Markets are watching close—and so should you.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment