A Federal Reserve interest rate cut—often simply called a “Fed rate cut”—is among the most watched events in global finance. Though technical in nature, a decision to lower the federal funds target rate ripples across the stock market, labor force, loan markets, and even global currency values. For households, businesses, and investors, understanding these impacts can be the difference between seizing an opportunity and missing the moment. In lately volatile years, such decisions have shifted trillions of dollars and rewritten economic forecasts in real time.

The Mechanics of a Fed Rate Cut

A Fed rate cut reduces the cost at which banks lend reserve funds to each other overnight. This “federal funds rate” serves as a foundational reference point for borrowing costs throughout the American—and global—financial system.

When the Federal Open Market Committee (FOMC) lowers its target rate, commercial banks can borrow more cheaply. This, in theory, incentivizes increased lending to businesses, consumers, and even other banks, fueling activity.

“Fed rate cuts are akin to opening the throttle on the U.S. economy—when applied judiciously, they can stimulate growth, encourage borrowing, and stabilize employment,” notes John Silvia, former chief economist at Wells Fargo.

Notably, these adjustments transmit into the economy at varying paces. While some effects on short-term market lending can be nearly immediate, broader consequences—such as housing demand or corporate expansion—can take months to unfold.

Market Dynamics: Stocks and Bonds React

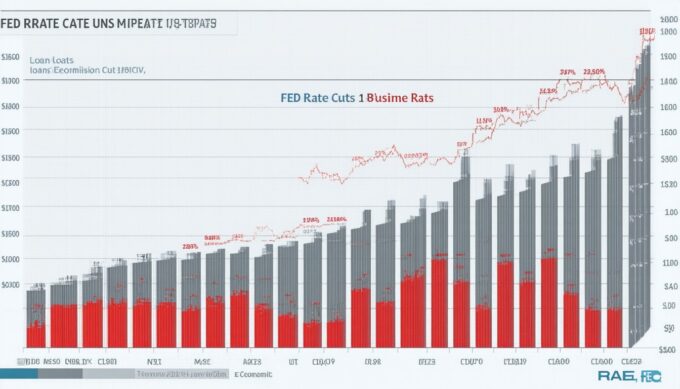

A Fed rate cut tends to galvanize the stock market, at least in the short run. Lower interest rates make borrowing less costly for companies, potentially boosting profits and, by extension, share prices. Growth sectors—like technology and real estate—often outperform when rates decline.

However, the relationship is nuanced:

- Positive Sentiment: Many investors view a rate cut as a sign that the Fed is committed to boosting growth, sparking rallies in equities.

- Yield Compression: Bond yields typically decline, as new bonds offer lower returns. This pushes some investors out of fixed income and into stocks in search of higher returns.

- Sector Winners and Losers: Rate-sensitive sectors (e.g., homebuilders, utilities, banks) move sharply after announcements. Banks can see margins squeezed due to narrowing spreads between deposit rates and loan yields.

In 2020, the pandemic-era emergency rate cuts provided a vivid real-world case. Stock indices initially wobbled on economic fears but ultimately surged as ultra-low rates, combined with fiscal stimulus, drove a hunt for yield and growth assets.

Individual Borrowing: Mortgages, Loans, and Credit Cards

Fed rate cuts have a downstream effect on borrowing costs for consumers:

Mortgage Rates

A lower fed funds rate filters into mortgage rates, though not perfectly or instantly. Thirty-year fixed mortgage rates generally track the yield of the 10-year Treasury bond, which tends to fall alongside the Fed funds target. This dynamic often leads to:

- A surge in refinancing activity as homeowners lock in lower rates

- Increased demand for home purchases, especially among first-time buyers

Consumer Loans and Credit Cards

Auto loans, personal loans, and credit card interest rates are all tied—directly or indirectly—to Fed policy. Lenders adjust rates based on their own costs of capital, which descend as the central bank cuts rates. While competitive loan products may see sharper rate reductions, card interest rates tend to lag and remain sticky due to risk and operational factors.

Economic Growth and Labor Markets

The theoretical aim of a Fed rate cut is to spur economic expansion. Businesses facing lower borrowing costs can:

- Finance expansion or new hiring more easily

- Invest in long-term projects with improved return prospects

Moreover, individuals may find it easier to access credit, increasing spending on durable goods, cars, or home renovations. Collectively, these activities can create a virtuous cycle: higher demand boosts sales and hiring, which in turn supports more demand.

Critically, rate cuts alone cannot resolve deep-rooted economic challenges. In times of financial crisis or when consumer confidence is low, easy money may only go so far. Nevertheless, the move is one of the most powerful tools for managing growth and employment.

Potential Downsides and Long-Term Risks

While rate cuts offer immediate relief and stimulus, they are not without risks:

- Asset Bubbles: Cheap borrowing can inflate prices in equities, housing, or commodities—raising fears of future corrections.

- Savings Erosion: Lower rates mean reduced yields for savers. For retirees or those relying on fixed income, this can be especially punitive.

- Currency Fluctuations: A rate cut often weakens the U.S. dollar by reducing its yield advantage, potentially making imports more expensive but aiding exporters.

In the ultra-low or zero-rate environments of the 2010s and early 2020s, many analysts voiced concerns over diminishing returns of additional easing. The longer rates remain suppressed, the more difficult it can become to normalize policy without roiling markets.

Real-World Scenarios: How Stakeholders Respond

Different groups experience Fed rate cuts in distinct ways:

- Investors may rotate portfolios toward riskier assets or income-generating stocks.

- Homebuyers and refinancers are incentivized to act quickly as mortgage rates drop.

- Banks see compressed net interest margins but can benefit from increased loan demand.

- Corporations accelerate borrowing for buybacks or capital expenditures.

In practice, timing is everything. Those who move early—refinancing mortgages or reallocating investments before moves become consensus—often fare best.

Strategic Considerations: When Does a Fed Rate Cut Matter Most?

Historically, the context of a rate cut shapes its impact:

- Preventive Cuts (when the Fed aims to head off a forecasted slowdown) can extend expansions and prop up asset prices.

- Reactive Cuts (amid crisis or recession) signal urgency, sometimes spooking markets or indicating deeper issues.

- Late-Cycle Cuts—when inflation or imbalances have already built up—carry risks of volatility and unintended consequences.

Policymakers must weigh near-term benefits against longer-term stability. As the post-2008 and post-2020 responses show, the magnitude and duration of cuts set the stage not just for economic recovery, but also for future policy constraints.

Conclusion: Navigating a Fed Rate Cut

The implications of a Fed rate cut are far-reaching, touching everything from Wall Street portfolios to Main Street wallets. While lower rates can boost borrowing, spur investment, and energize markets, they also carry risks that must be managed by investors, businesses, and policymakers alike. Staying informed about both immediate and downstream effects remains crucial, whether you’re refinancing a mortgage, allocating investments, or making business decisions in a shifting economic landscape.

FAQs

How quickly does a Fed rate cut impact mortgage rates?

Mortgage rates often begin to move in anticipation of a Fed rate cut but typically adjust more noticeably within a few weeks after the decision. The alignment is not precise, as these rates also reflect long-term bond yields and investor sentiment.

Do rate cuts always boost the stock market?

Not necessarily. While lower rates can provide stimulus and encourage risk-taking, markets may sometimes interpret cuts as a sign of underlying economic trouble. The context and investor expectations are crucial.

What happens to savings accounts when the Fed cuts rates?

Savings account yields usually decline after the Fed acts, as banks lower the interest they pay to depositors. This often makes it harder for savers to generate meaningful returns from traditional accounts.

Why might a Fed rate cut not work as intended?

If consumers or businesses remain cautious—due to uncertain job prospects or broader economic fears—cheaper borrowing may not translate into greater spending or investment. Additionally, structural issues cannot be resolved by rates alone.

Are some loans unaffected by Fed rate cuts?

Certain fixed-rate loans, especially those locked in before rate changes, will not reprice until renewal. Some lenders may also choose not to pass on the full reduction, based on risk appetites or funding sources.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment