The debate over whether US stablecoins are becoming central bank digital currencies in all but name has intensified as Washington moves from theory to law. Since the GENIUS Act was signed in July 2025, the United States has given dollar-backed stablecoins a formal regulatory framework while the Federal Reserve continues to say it has made no decision to issue a US CBDC. That split appears clear on paper. In practice, however, the policy goals, oversight mechanisms, and payment ambitions of stablecoins and CBDCs are starting to overlap in ways that deserve closer scrutiny.

A debate that has moved from crypto circles to Washington

For years, stablecoins were treated mainly as tools for crypto trading. That is changing. Federal Reserve Governor Michael Barr said in October 2025 that stablecoins have the potential to improve payment efficiency, especially in cross-border use, if regulators build strong guardrails and consumer protections around them. Federal Reserve Governor Christopher Waller has also argued that stablecoins are a form of private money that could support payments innovation if they are regulated in a way that addresses their specific risks.

That shift matters because the US government is no longer discussing stablecoins only as speculative crypto instruments. Treasury Secretary Scott Bessent said after the GENIUS Act became law on July 18, 2025, that stablecoins give the dollar an “internet-native payment rail” and could increase demand for US Treasuries. The Treasury’s framing places stablecoins closer to national payments infrastructure than to a niche corner of digital assets.

The market’s scale adds urgency. CoinGecko reported that total stablecoin market capitalization ended 2025 at about $311 billion, up nearly 49% year over year. A market of that size is no longer easy for policymakers to treat as peripheral.

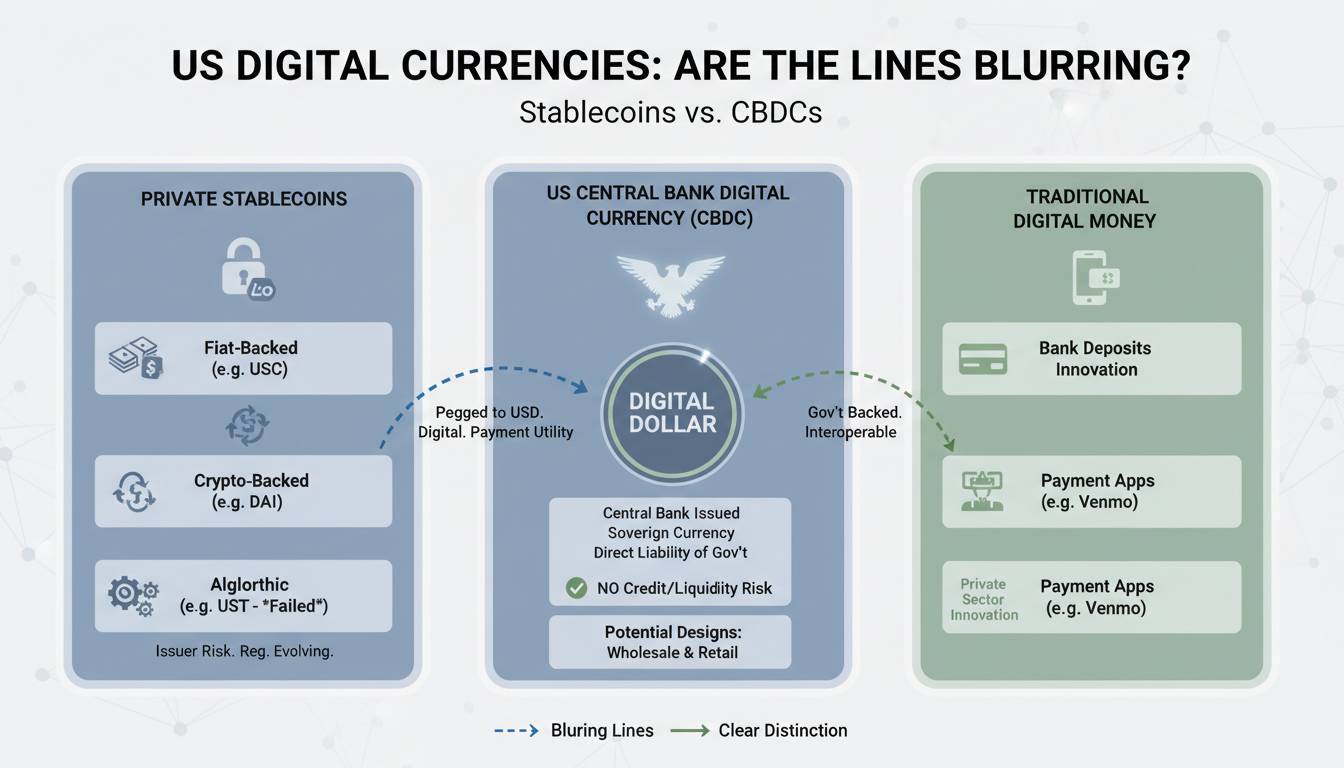

Are US stablecoins just CBDCs in disguise? Look closely and the differences start to blur

The traditional distinction is simple. A CBDC is a digital liability of the central bank. A stablecoin is a digital token issued by a private company, usually backed by reserves such as cash and short-term Treasuries. On that definition alone, they are not the same thing. Federal Reserve officials have repeatedly described stablecoins as private money, while also stating that the Fed would need clear support from the executive branch and authorizing legislation from Congress before issuing a CBDC.

Yet the differences begin to blur when the focus shifts from legal form to economic function. Both instruments aim to deliver digital dollars that move quickly across networks. Both are discussed as tools for modernizing payments, improving cross-border transfers, and preserving the international role of the dollar. Waller said in February 2025 that dollar stablecoins could appeal to users in high-inflation countries or to people without easy access to dollar cash or banking services. Treasury has framed regulated stablecoins as a way to extend the dollar economy globally.

In other words, the public policy case once used to justify a CBDC is increasingly being applied to regulated private issuers instead. That does not make stablecoins CBDCs in a legal sense. It does mean they may serve some of the same strategic purposes.

Where the similarities are strongest

The overlap is most visible in four areas:

- Digital dollar access: Both CBDCs and dollar stablecoins are designed to provide digital representations of the US dollar.

- Payments modernization: Federal Reserve officials have pointed to stablecoins’ possible role in faster and cheaper payments, especially across borders.

- State-backed policy goals: Treasury has explicitly linked stablecoins to dollar dominance and Treasury demand.

- Regulatory integration: The GENIUS Act moved stablecoins deeper into the supervised financial system, narrowing the gap between private issuance and public oversight.

This is why critics argue that heavily regulated stablecoins could become a privatized version of a CBDC model. If issuers must meet reserve, compliance, redemption, and supervisory standards set by federal authorities, the token may remain privately issued while operating inside a public-policy perimeter.

The differences still matter

Even with that convergence, the differences are not cosmetic. A CBDC would be a direct claim on the Federal Reserve. A stablecoin remains a claim on an issuer whose safety depends on reserves, governance, operations, and regulation. Barr has warned that stablecoins need guardrails because payment innovation can create risks for households, businesses, and the broader financial system. Waller has also emphasized that stablecoin risks are not identical to bank risks and should be regulated directly and proportionately.

That distinction affects several core issues:

Credit and run risk

A CBDC, if issued by the Fed, would generally be viewed as free of private issuer credit risk. Stablecoins are not. Federal Reserve officials have repeatedly noted that stablecoins can face run risk and depegging risk. That is one reason US lawmakers moved to create a formal framework for payment stablecoins.

Governance and accountability

A CBDC would sit within the central bank and, in the US case, would require political authorization. Stablecoins are governed by private firms, even if those firms are supervised. That means product design, distribution, and commercial incentives remain partly in private hands.

Competition and market structure

Waller has argued that regulation should allow both banks and nonbanks to issue stablecoins. That is very different from a single public issuer model. A CBDC could centralize digital dollar issuance. Stablecoins create a competitive field, though one shaped by regulation.

Why the political argument is getting sharper

The phrase “CBDC in disguise” has political force because it captures a broader concern: that digital money can become more traceable, more programmable, and more dependent on state-approved intermediaries even without a formal CBDC launch. That concern is not entirely theoretical. Stablecoin issuers already operate under anti-money-laundering, sanctions, and law-enforcement compliance expectations, and lawmakers have pushed for stronger oversight of foreign issuers and domestic operators.

Supporters answer that this is precisely the point. They argue that if digital dollars are going to scale, they need legal certainty, reserve standards, redemption rights, and compliance controls. In that view, regulated stablecoins are not disguised CBDCs. They are a market-based alternative to one.

According to Michael Barr, the key question is whether the regulatory framework creates strong enough guardrails to let innovation improve payments without creating unacceptable risks. According to Christopher Waller, the public sector’s role is to set fair rules while allowing the private sector to build useful products. Those positions suggest the Fed sees regulated stablecoins less as a stealth CBDC and more as supervised private money.

What it means for banks, fintechs, and consumers

For banks, the rise of regulated stablecoins could mean new competition in payments and deposits, but also new opportunities in tokenized money and settlement. Barr said in 2025 that market participants and regulators may need to consider how tokenized deposits fit into the broader ecosystem. That signals that stablecoins are now part of a larger redesign of digital finance, not a standalone crypto issue.

For fintech firms and nonbank issuers, the GENIUS Act offers legitimacy but also tighter obligations. The tradeoff is straightforward: more access to the mainstream financial system in exchange for more supervision.

For consumers, the outcome is more mixed. Regulated stablecoins may offer faster transfers and broader digital dollar access. But they do not eliminate questions around privacy, platform dependence, or the concentration of payment power in a handful of large issuers and regulated intermediaries.

The bigger picture for the dollar

The strongest case for stablecoins is geopolitical as much as technological. Treasury has argued that they can reinforce the dollar’s reserve-currency role and expand access to the dollar economy worldwide. Waller has similarly highlighted the appeal of dollar stablecoins abroad. If that vision succeeds, the US may achieve many of the international benefits associated with a CBDC without the Federal Reserve ever issuing one directly.

That is why the lines are blurring. The legal architecture still separates stablecoins from CBDCs. The strategic outcome may not be so different.

Conclusion

US stablecoins are not CBDCs in the strict legal sense. They are privately issued digital dollars, not direct liabilities of the Federal Reserve. But as regulation tightens and policymakers increasingly treat them as instruments of payments modernization, dollar distribution, and financial strategy, the functional gap is narrowing. The real question is no longer whether stablecoins and CBDCs are identical. It is whether Americans will care about that distinction if both systems ultimately deliver a highly supervised, internet-native dollar.

Frequently Asked Questions

What is the main difference between a stablecoin and a CBDC?

A stablecoin is typically issued by a private company and backed by reserves. A CBDC would be issued directly by a central bank and would be a central bank liability.

Did the US launch a CBDC?

No. The Federal Reserve has said it has made no decision to issue a CBDC and would only move forward with clear executive support and authorizing legislation from Congress.

What changed for stablecoins in 2025?

The GENIUS Act was signed into law on July 18, 2025, creating a federal framework for payment stablecoins in the United States.

Why do some people say stablecoins are CBDCs in disguise?

They argue that once stablecoins are tightly regulated and integrated into national payment policy, they can serve many of the same functions as a CBDC even if private firms issue them.

How large is the stablecoin market now?

CoinGecko reported that total stablecoin market capitalization reached about $311 billion at the end of 2025.

Why do policymakers support regulated stablecoins?

Supporters say they can improve payment efficiency, support cross-border transfers, expand access to digital dollars, and strengthen the global role of the US dollar if proper safeguards are in place.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment